How Geography Impacts The Offtake Strategies Of The Winners Of The Latest European Hydrogen Bank Auction

Time to read:

5

mins

Analysis by VNZ Insights shows how each project plans to deliver its hydrogen or derivatives to end customers, revealing how geography shapes offtake strategies across Europe’s fast-growing green energy market. This analysis was originally published on Hydrogen Insight on 7 August 2025, authored by Polly Martin and Amish Singh.

Context: The European Hydrogen Bank Auction Landscape

The European Hydrogen Bank’s second auction, announced earlier this year, drew diverse bids from across the continent, each with distinct strategies to produce, transport, and deliver hydrogen. But what determines these offtake choices? According to VNZ Insights, the answer often lies in geography : from existing pipeline infrastructure to access to ports and industrial clusters.

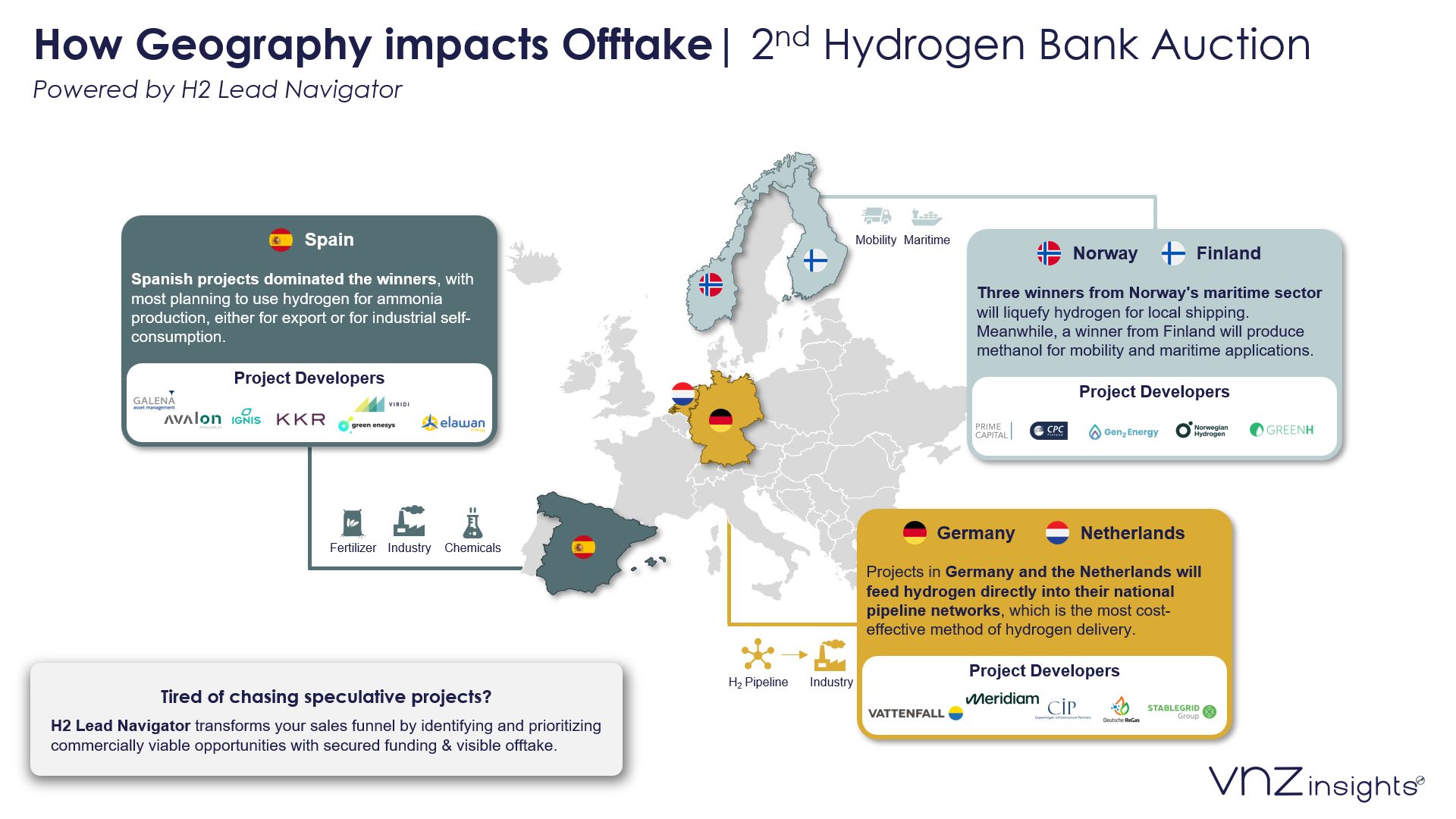

Northern Europe: Pipeline Advantage

Projects in Germany and the Netherlands, such as the 560MW Zeevonk Electrolyser and 368MW Kaskade facility, plan to feed hydrogen directly into their national pipeline networks — currently the cheapest and most scalable method of hydrogen delivery.

With hydrogen backbone networks already under construction in both countries, these projects benefit from early infrastructure readiness and policy alignment.

Nordics: Turning Hydrogen into Maritime Fuel

In Finland, the 200MW Kristinestad PtX project is taking a different route — converting hydrogen into methanol. This can be used directly as a maritime fuel or as a precursor for e-gasoline exports to Germany.

Meanwhile, all three Norwegian projects in the maritime-exclusive auction bucket plan to liquefy hydrogen for local shipping use, reinforcing Norway’s position as a leader in green maritime energy.

Southern Europe: Split Strategies in Spain

Spain, home to the majority of auction winners, presents a more fragmented picture. This is largely due to infrastructure uncertainty, as the country’s national hydrogen backbone is not expected to be operational until 2027.

The larger projects, such as 252MW Villamartin H2 and 98MW Puerto Serrano H2, aim to produce ammonia for export to Northern Europe, a stable and transportable hydrogen derivative. By contrast, the 80MW SolWinHy Cadiz project focuses on methanol feedstock for e-fuels, already securing export agreements to Germany.

Smaller Spanish projects (30MW and below) intend to supply co-located industrial users directly or have yet to disclose transport details — a sign of logistical uncertainty in Spain’s hydrogen ecosystem.

Infrastructure Gaps and Price Trends

A previous auction winner, DH2 Energy, noted that Spain lacks infrastructure for molecule transport and support for compressed hydrogen trailers — a key barrier for distributed hydrogen delivery.

Interestingly, while the lowest bid price dropped by 85% from €0.37/kg to €0.20/kg between the first and second auctions, the volume-weighted average remained almost constant (€0.46/kg → €0.44/kg).

This signals greater price competitiveness but similar cost baselines across projects.

Find All These Details & Projects On VNZ H2 Lead Navigator

VNZ Insights recently launched the H2 Lead Navigator Tool, offering a data-driven view of Europe’s green hydrogen pipeline.

It helps OEMs, investors, and EPCs identify high-potential projects, understand regional infrastructure readiness, and map offtake risks tied to geography.Download the insight/report:

Sources-

https://www.hydrogeninsight.com/production/how-geography-impacts-the-offtake-strategies-of-the-winners-of-the-latest-european-hydrogen-bank-auction/2-1-1854757

Image Sources-